Maximizing 2026 Retirement Contributions: IRS Limits & Strategies

Anúncios

Maximizing Your 2026 Retirement Contributions: Unpacking New IRS Limits and Strategies for U.S. Savers

As we navigate the ever-evolving landscape of personal finance, planning for retirement remains a cornerstone of long-term financial security. For U.S. savers, understanding and strategically utilizing annual retirement contribution limits is paramount. The year 2026 brings with it potential adjustments to these limits, set by the Internal Revenue Service (IRS), which can significantly impact your ability to build a robust nest egg. This comprehensive guide will delve into the anticipated 2026 Retirement Contributions, offering insights into the various account types, the impact of inflation, and actionable strategies to help you maximize your savings.

Anúncios

The journey to a comfortable retirement is a marathon, not a sprint. Each year presents new opportunities to optimize your savings, and 2026 will be no exception. By proactively understanding the nuances of IRS regulations and employing smart financial planning, you can ensure you’re on the fast track to achieving your retirement dreams. We’ll explore everything from traditional 401(k)s and IRAs to specialized accounts like SEP IRAs and SIMPLE IRAs, providing a holistic view of the options available to you.

Understanding the Importance of Annual Contribution Limits

Annual contribution limits are more than just numbers; they represent the maximum amounts you can contribute to various tax-advantaged retirement accounts each year. These limits are periodically adjusted by the IRS, primarily to account for inflation and cost-of-living increases. While the official 2026 Retirement Contributions limits are typically announced in late fall of the preceding year (i.e., late 2025), we can make educated projections based on historical trends and economic forecasts.

Anúncios

Why are these limits so crucial? Because contributing the maximum allowed amount each year can significantly accelerate your retirement savings. Tax-advantaged accounts offer benefits such as tax-deferred growth (for traditional accounts) or tax-free withdrawals in retirement (for Roth accounts), which can translate into substantial savings over decades. Missing out on these opportunities means leaving potential growth and tax benefits on the table.

Moreover, consistently contributing up to the limit instills financial discipline and helps you stay on track with your retirement goals. It forces you to prioritize long-term savings, which is essential for combating inflation and ensuring you have sufficient funds to cover your expenses during your non-working years. The power of compound interest works best when you contribute consistently and maximize your contributions early and often.

Projected 2026 Retirement Contributions for Key Account Types

While we await the official IRS announcements, we can anticipate the likely increases for 2026 Retirement Contributions across the most common retirement vehicles. These projections are based on current economic indicators, including inflation rates and cost-of-living adjustments (COLAs).

401(k), 403(b), and TSP Plans

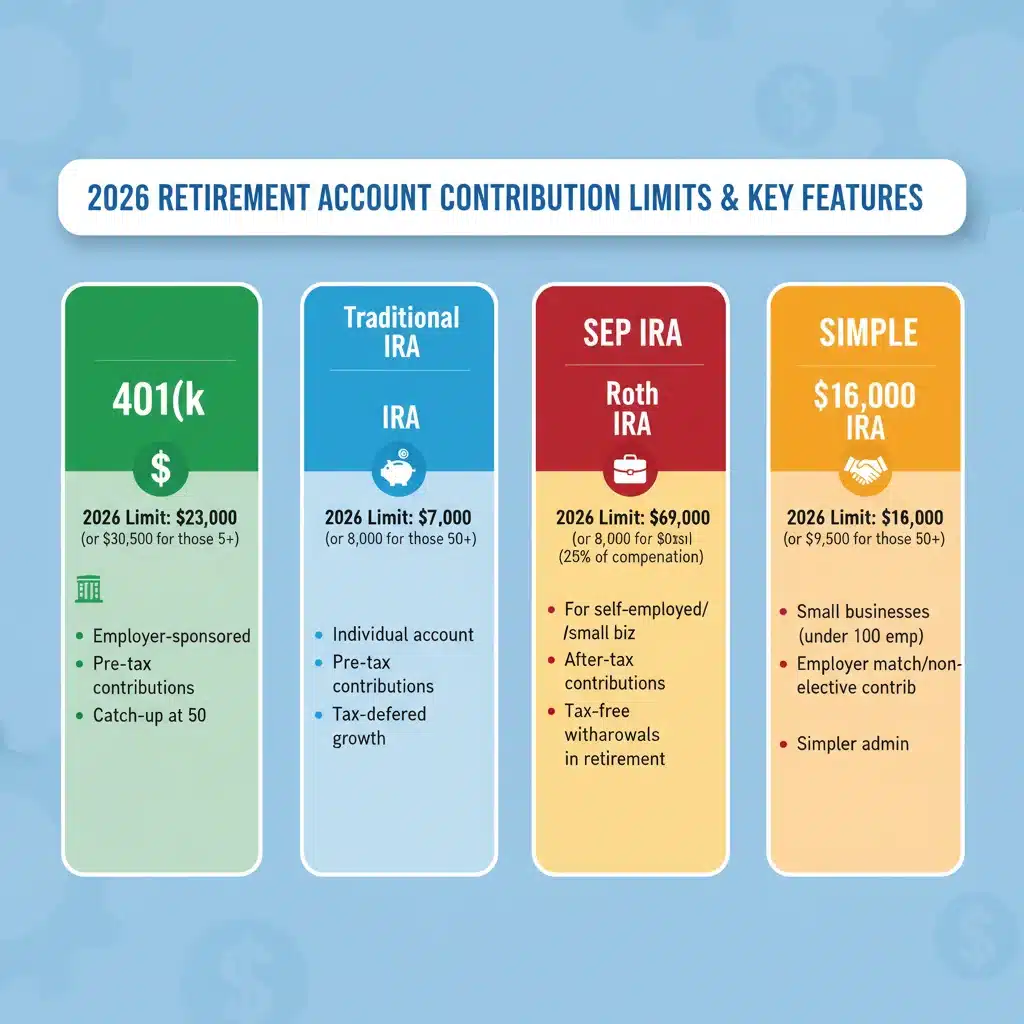

Employer-sponsored plans like 401(k)s, 403(b)s, and the Thrift Savings Plan (TSP) are often the bedrock of many individuals’ retirement savings. The contribution limits for these plans are usually the highest among individual accounts, reflecting their primary role in workplace savings. For 2025, the elective deferral limit for these plans is $23,000. Historically, these limits have seen incremental increases year over year.

Given projected inflation, it’s reasonable to expect the 2026 Retirement Contributions limit for 401(k)s, 403(b)s, and TSP plans to rise. A conservative estimate might place this limit in the range of $23,500 to $24,500. This increase, though seemingly small annually, accumulates significantly over a working career. For instance, an extra $500 contributed each year for 30 years, assuming an 8% annual return, could add tens of thousands of dollars to your retirement nest egg.

IRA and Roth IRA Contributions

Individual Retirement Arrangements (IRAs) and Roth IRAs are popular choices for those without employer-sponsored plans or for those looking to supplement their workplace savings. These accounts offer flexibility and a wide range of investment options. The 2025 IRA contribution limit is $7,000.

Similar to 401(k)s, the 2026 Retirement Contributions limit for IRAs and Roth IRAs is also likely to see an increase. We could anticipate this limit to move into the $7,500 range. It’s crucial to remember that income limitations apply to Roth IRA contributions and the deductibility of traditional IRA contributions. High-income earners might be phased out of direct Roth IRA contributions but can still utilize the ‘backdoor Roth’ strategy, which we’ll discuss later.

Catch-Up Contributions for Savers Age 50 and Over

Recognizing that many individuals start saving later in life or wish to accelerate their savings as they approach retirement, the IRS allows for ‘catch-up contributions’ for those aged 50 and over. These additional contributions can be made on top of the standard limits, providing a significant boost to retirement funds.

For 2025, the catch-up contribution limit for 401(k)s, 403(b)s, and TSP plans is $7,500, and for IRAs, it’s $1,000. These limits are also subject to inflation adjustments. For 2026 Retirement Contributions, we might see the 401(k) catch-up limit nudge slightly higher, perhaps to $8,000, while the IRA catch-up limit might remain stable or see a minor increase. These catch-up provisions are incredibly valuable and should be utilized by eligible individuals to supercharge their savings.

SEP IRA and SIMPLE IRA Contributions

For self-employed individuals and small business owners, SEP IRAs (Simplified Employee Pension) and SIMPLE IRAs (Savings Incentive Match Plan for Employees) offer excellent retirement savings opportunities. The limits for these accounts are often tied to a percentage of compensation or a specific dollar amount, both of which are adjusted annually.

- SEP IRA: The maximum contribution to a SEP IRA for an employee (including a self-employed individual) is generally the lesser of 25% of compensation or a specific dollar amount, which for 2025 is $69,000. For 2026 Retirement Contributions, this dollar limit is expected to increase, potentially reaching $70,000 or more, offering significant savings potential for high-income self-employed individuals.

- SIMPLE IRA: For 2025, the SIMPLE IRA contribution limit is $16,000, with an additional catch-up contribution of $3,500 for those age 50 and over. These limits are also very likely to see an increase for 2026 Retirement Contributions, possibly to $16,500 for regular contributions and $4,000 for catch-up contributions.

Understanding these specialized plans is crucial for small business owners and independent contractors, as they offer unique advantages and higher contribution ceilings compared to traditional IRAs.

Strategies to Maximize Your 2026 Retirement Contributions

Knowing the limits is only half the battle; the other half is implementing effective strategies to meet or exceed them. Here are several actionable approaches to help you maximize your 2026 Retirement Contributions:

1. Automate Your Savings

One of the simplest yet most effective strategies is to automate your contributions. Set up automatic deductions from your paycheck into your 401(k) or automatic transfers from your checking account to your IRA. This ‘set it and forget it’ approach ensures consistency and reduces the temptation to spend money that could be saved. As the 2026 Retirement Contributions limits are announced, adjust your automatic contributions to reflect the new maximums.

2. Take Advantage of Employer Matches

If your employer offers a matching contribution to your 401(k) or 403(b), always contribute at least enough to receive the full match. This is essentially free money and provides an immediate, guaranteed return on your investment. Failing to do so means leaving money on the table, which is a missed opportunity for your retirement savings.

3. Prioritize High-Interest Debt Repayment (Strategically)

While it might seem counterintuitive to prioritize debt repayment over retirement contributions, high-interest debt (like credit card debt) can erode your financial progress. A balanced approach involves making minimum payments on high-interest debt while still contributing enough to your retirement accounts to get any employer match. Once high-interest debt is under control, you can then redirect those funds towards maximizing your 2026 Retirement Contributions.

4. Utilize the ‘Backdoor Roth’ Strategy

For high-income earners who exceed the income limits for direct Roth IRA contributions, the ‘backdoor Roth’ strategy can be a valuable tool. This involves contributing to a traditional IRA (which has no income limits for non-deductible contributions) and then immediately converting it to a Roth IRA. While there are some tax implications to consider, a qualified financial advisor can help you navigate this strategy to effectively increase your Roth savings.

5. Consider a Health Savings Account (HSA)

While primarily a healthcare savings vehicle, an HSA is often referred to as a ‘triple tax-advantaged’ account and can serve as an excellent supplemental retirement savings tool. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Once you reach age 65, you can withdraw funds for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income. For 2026 Retirement Contributions, the HSA limits are also expected to increase, making it an even more attractive option for eligible individuals.

6. Maximize Catch-Up Contributions

If you are age 50 or older, do everything you can to take advantage of catch-up contributions. These additional contributions can significantly boost your retirement savings in the years leading up to retirement, helping you compensate for any periods where you might have under-contributed or simply accelerating your path to financial independence. The extra $7,500 or $1,000 (or more, depending on 2026 limits) can make a substantial difference over a few years.

7. Review Your Asset Allocation

Beyond just contributing, ensure your investments within your retirement accounts are appropriately allocated based on your risk tolerance and time horizon. As you approach 2026 Retirement Contributions, it’s a good time to review your portfolio. A well-diversified portfolio, strategically aligned with your goals, can help maximize growth potential while managing risk, ultimately enhancing the value of your contributions.

8. Plan for Windfalls and Bonuses

Unexpected income, such as bonuses, tax refunds, or inheritances, presents a golden opportunity to supercharge your retirement savings. Instead of spending these windfalls, consider directing a significant portion towards maximizing your 2026 Retirement Contributions. This can help you hit the annual limits without impacting your regular budget.

The Impact of Inflation on Your 2026 Retirement Contributions

Inflation is a critical factor in determining the actual purchasing power of your retirement savings. The IRS adjusts contribution limits periodically precisely to account for inflation, ensuring that the real value of your contributions remains relatively consistent over time. However, even with these adjustments, it’s essential to understand how inflation can erode your future purchasing power.

For example, if the cost of living continues to rise, the same dollar amount in retirement will buy less than it does today. This is why maximizing your 2026 Retirement Contributions and ensuring your investments are growing at a rate that outpaces inflation is so vital. Diversifying your portfolio with a mix of assets that historically perform well during inflationary periods, such as real estate or inflation-protected securities, can be a prudent strategy.

Furthermore, inflation impacts not only the cost of goods and services but also healthcare expenses, which are often a significant concern in retirement. By consistently contributing the maximum to your retirement accounts and considering an HSA, you’re building a buffer against the rising costs of living and healthcare in your golden years.

Understanding the Tax Implications of Your Choices

The tax treatment of your retirement contributions is a major advantage of utilizing these accounts. Understanding the differences between pre-tax and after-tax contributions is crucial for effective planning.

- Traditional 401(k) / IRA: Contributions are typically made on a pre-tax basis, meaning they reduce your taxable income in the year they are made. Your investments grow tax-deferred, and you pay taxes on your withdrawals in retirement. This can be advantageous if you expect to be in a lower tax bracket in retirement than you are during your working years.

- Roth 401(k) / Roth IRA: Contributions are made with after-tax dollars, meaning they do not reduce your current taxable income. However, your investments grow tax-free, and qualified withdrawals in retirement are also tax-free. This is often beneficial if you expect to be in a higher tax bracket in retirement or if you want to diversify your tax exposure in retirement.

When planning your 2026 Retirement Contributions, consider your current and projected future tax brackets. A mix of both traditional and Roth accounts can offer flexibility and help you manage your tax burden in retirement. Consulting with a tax professional can provide personalized advice based on your specific financial situation.

Resources and Tools for Retirement Planning

To effectively plan and track your 2026 Retirement Contributions, several resources and tools are available:

- Financial Advisors: A certified financial planner (CFP) can provide personalized advice, help you set realistic goals, and develop a comprehensive retirement plan tailored to your needs. They can also assist with complex strategies like the backdoor Roth.

- Online Retirement Calculators: Many financial websites offer free retirement calculators that can help you estimate how much you need to save and project the growth of your investments based on various contribution scenarios.

- Employer Benefits Portals: If you have an employer-sponsored plan, your company’s benefits portal will provide details on your plan, contribution options, and investment choices.

- IRS Website: The official IRS website is the definitive source for current and past contribution limits, as well as detailed information on retirement plans and tax rules. Keep an eye on their announcements for the official 2026 Retirement Contributions limits.

Staying Informed About Future Changes

The financial landscape is dynamic, and retirement rules and limits can change. It’s crucial to stay informed about any legislative changes or economic shifts that might impact your retirement planning. Subscribe to financial news outlets, follow reputable financial blogs, and regularly check the IRS website for updates on 2026 Retirement Contributions and beyond.

Proactive engagement with your retirement plan is a continuous process. Don’t just set it and forget it entirely; rather, review your strategy annually, especially as new contribution limits are announced. This allows you to make timely adjustments to your savings rates and investment allocations, ensuring you remain on track for a secure and comfortable retirement.

Conclusion: Take Control of Your 2026 Retirement Contributions

Maximizing your 2026 Retirement Contributions is a critical step towards securing your financial future. By understanding the anticipated IRS limits for 401(k)s, IRAs, and other retirement accounts, and by implementing smart savings strategies, you can significantly boost your retirement nest egg. Whether you’re just starting your career or nearing retirement, every contribution counts, and maximizing those contributions, especially for those aged 50 and over utilizing catch-up provisions, can make a profound difference.

Don’t wait for the official announcements to start planning. Begin by reviewing your current savings, assessing your financial goals, and preparing to adjust your contributions as soon as the 2026 Retirement Contributions limits are released. With diligent planning and consistent effort, you can look forward to a retirement filled with financial peace of mind and the freedom to enjoy the fruits of your labor.

Remember, your future self will thank you for the efforts you make today. Start maximizing your 2026 retirement contributions now!

& IRA Limits in the US")

Matching Over 5 Years?")