Mastering Tax-Loss Harvesting for 2026: Optimize Your Portfolio Now

As investors look ahead to 2026, proactive financial planning becomes paramount. One of the most powerful, yet often underutilized, strategies in an investor’s toolkit is Tax-Loss Harvesting 2026. This sophisticated technique allows you to reduce your taxable income by strategically selling investments at a loss, offsetting capital gains, and even a portion of ordinary income. With the December deadline for 2026 rapidly approaching, understanding and implementing effective tax-loss harvesting strategies can significantly enhance your after-tax returns and overall portfolio health.

Anúncios

The financial landscape is constantly evolving, making it crucial for investors to stay informed about tax laws and their implications. By actively engaging in Tax-Loss Harvesting 2026, you’re not just saving on taxes; you’re also refining your portfolio, rebalancing, and positioning yourself for future growth. This comprehensive guide will delve into the intricacies of tax-loss harvesting, providing you with actionable insights, critical rules to follow, and a roadmap to optimize your investment strategy before the year ends.

Many investors shy away from tax-loss harvesting, viewing it as overly complex or time-consuming. However, with the right knowledge and a clear plan, it can become a routine part of your annual financial review, yielding substantial benefits. We’ll break down the core concepts, explore the benefits, and highlight common pitfalls to avoid, ensuring you are well-equipped to make informed decisions for your 2026 tax year.

Anúncios

What is Tax-Loss Harvesting and Why is it Crucial for 2026?

At its core, tax-loss harvesting involves selling investments that have lost value to realize a capital loss. These realized losses can then be used to offset any capital gains you may have incurred from selling other investments at a profit. If your capital losses exceed your capital gains, you can use up to $3,000 of the remaining loss to offset your ordinary income each year. Any unused capital losses can be carried forward indefinitely to offset future capital gains or ordinary income.

The significance of Tax-Loss Harvesting 2026 cannot be overstated. In volatile markets, investors often find themselves with holdings that have declined in value. While no one enjoys seeing their investments dip, these dips present a unique opportunity for tax optimization. By strategically selling these underperforming assets, you convert a paper loss into a realized tax benefit. This not only reduces your current tax bill but can also improve the portfolio’s long-term performance by freeing up capital to reinvest in more promising opportunities.

Consider a scenario where you’ve realized $10,000 in capital gains from selling a high-performing stock. Simultaneously, you hold another stock that has dropped by $7,000. By harvesting that $7,000 loss, you can reduce your taxable capital gains from $10,000 to $3,000, leading to significant tax savings. If you have no capital gains to offset, that $7,000 loss could offset $3,000 of your ordinary income, and the remaining $4,000 would carry forward to future years. This flexibility makes Tax-Loss Harvesting 2026 a powerful tool for managing your tax exposure.

The end of the year, typically by December 31st, is the critical deadline for realizing losses in the current tax year. This means that for Tax-Loss Harvesting 2026, you must execute your trades before the final trading day of December 2026. Procrastination can lead to missed opportunities, so understanding the timeline and planning ahead are essential.

The Mechanics of Tax-Loss Harvesting: A Step-by-Step Approach

Implementing Tax-Loss Harvesting 2026 effectively requires a clear, methodical approach. Here’s a breakdown of the steps involved:

Step 1: Identify Underperforming Assets

Begin by reviewing your investment portfolio to identify assets that are currently trading below their purchase price. These are your potential candidates for tax-loss harvesting. Look for individual stocks, bonds, mutual funds, or ETFs that have experienced a significant decline in value since you acquired them. It’s important to consider both short-term and long-term losses, as they offset different types of gains.

Step 2: Calculate Your Capital Gains and Losses

Before you sell, get a clear picture of your current capital gains and losses. Your brokerage statements will provide this information. Sum up all realized gains and losses for the year to understand your net position. This will help you determine how many losses you need to harvest to achieve your desired tax outcome. Remember, short-term losses (assets held for one year or less) offset short-term gains first, and long-term losses (assets held for more than one year) offset long-term gains first. Any remaining losses can then offset other types of gains.

Step 3: Execute the Sale

Once you’ve identified the assets and calculated the potential impact, execute the sale of the underperforming investments. This action formally realizes the capital loss. Ensure these transactions are completed before the December 2026 deadline to count for the current tax year.

Step 4: Reinvest (Carefully!)

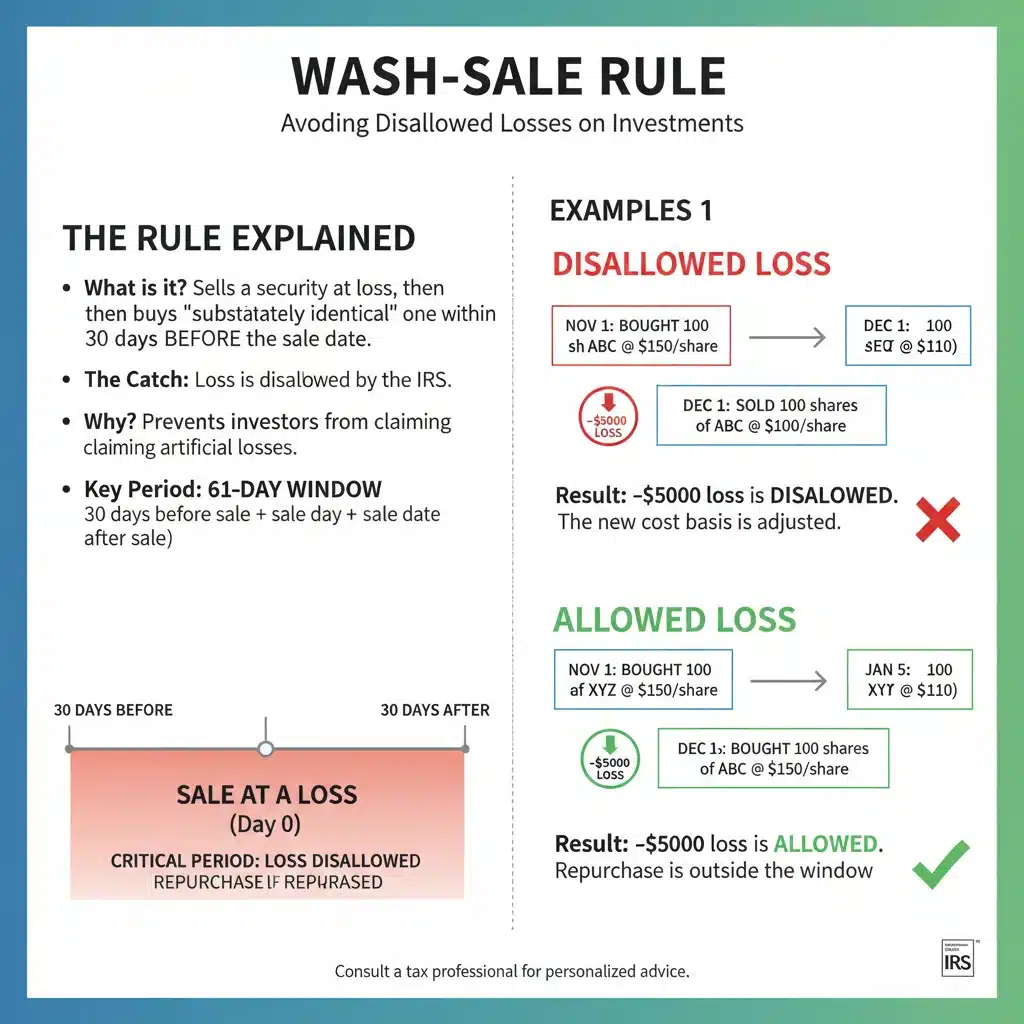

After selling an asset for a loss, you might want to reinvest the proceeds. However, this is where the notorious ‘wash-sale rule’ comes into play. The wash-sale rule prohibits you from claiming a loss if you buy a substantially identical security within 30 days before or after the sale. This 61-day window (30 days before, the day of sale, and 30 days after) is crucial to remember. If you violate this rule, your loss will be disallowed.

To avoid a wash sale, you have several options:

- Wait it out: Simply wait more than 30 days to repurchase the same security.

- Buy a different security: Reinvest in a similar, but not substantially identical, security. For example, if you sell an S&P 500 index ETF, you could buy a total market index ETF or a different S&P 500 ETF from a different provider.

- Do nothing: Hold the cash for now if you don’t immediately see a suitable alternative investment.

Understanding the Wash-Sale Rule: A Critical Component of Tax-Loss Harvesting 2026

The wash-sale rule is perhaps the most important regulation to understand when engaging in Tax-Loss Harvesting 2026. Its purpose is to prevent investors from claiming artificial losses by selling a security and immediately repurchasing it, effectively maintaining their investment position while realizing a tax benefit. The rule states that if you sell a security for a loss and then buy a ‘substantially identical’ security within 30 days before or after the sale date, the loss is disallowed.

What constitutes ‘substantially identical’? This is where it can get tricky. Generally, it refers to the same stock or bond. For mutual funds and ETFs, it typically means funds with the same investment objectives and underlying holdings. For instance, selling an S&P 500 ETF from Vanguard and immediately buying an S&P 500 ETF from iShares would likely trigger the wash-sale rule because they track the same index and are considered substantially identical.

Consequences of a wash sale: If a wash sale occurs, the disallowed loss is not lost forever. Instead, it is added to the cost basis of the newly acquired substantially identical security. This means that when you eventually sell the new security, your cost basis will be higher (by the amount of the disallowed loss), which will reduce your capital gain or increase your capital loss at that future date. While the loss isn’t permanently gone, its immediate tax benefit is deferred, defeating the purpose of current-year Tax-Loss Harvesting 2026.

To navigate the wash-sale rule successfully, meticulous record-keeping is vital. Keep track of all your buy and sell dates, especially around your tax-loss harvesting activities. If you use multiple brokerage accounts, remember that the wash-sale rule applies across all accounts, including those of your spouse if you file jointly. Automated tax-loss harvesting services offered by robo-advisors often have built-in mechanisms to avoid wash sales, which can be a significant advantage for hands-off investors.

Benefits Beyond Tax Savings for Tax-Loss Harvesting 2026

While the primary motivation for Tax-Loss Harvesting 2026 is undoubtedly tax reduction, the strategy offers several other compelling benefits that contribute to overall portfolio optimization:

Portfolio Rebalancing and Risk Management

Selling underperforming assets provides an excellent opportunity to rebalance your portfolio. If certain sectors or asset classes have performed poorly, harvesting those losses allows you to shed undesirable holdings and reinvest in areas that align better with your current investment goals and risk tolerance. This systematic review helps maintain your desired asset allocation and can reduce concentration risk within your portfolio.

Improved Investment Discipline

Regularly reviewing your portfolio for tax-loss harvesting opportunities encourages a disciplined approach to investing. It forces you to assess the performance of your holdings, differentiate between temporary dips and fundamental weaknesses, and make strategic decisions rather than emotional ones. This discipline can lead to better long-term investment outcomes.

Enhanced After-Tax Returns

By effectively managing your tax liabilities, you increase your net returns. The money saved on taxes can be reinvested, compounding over time and potentially leading to significant wealth accumulation. This is the core principle of tax efficiency: it’s not just about what you earn, but what you keep after taxes.

Flexibility with Carried-Forward Losses

The ability to carry forward unused capital losses indefinitely is a powerful feature. This means that even if you don’t have enough capital gains or ordinary income to offset in 2026, those losses will remain available to reduce your tax burden in future years. This provides a long-term tax benefit that can be strategically deployed when market conditions or your financial situation change.

Common Pitfalls to Avoid When Implementing Tax-Loss Harvesting 2026

Despite its benefits, Tax-Loss Harvesting 2026 comes with potential traps that investors must navigate carefully:

Ignoring the Wash-Sale Rule

As discussed, this is the most common mistake. Accidentally repurchasing a substantially identical security within the 61-day window will invalidate your harvested loss. Always double-check your transactions and consider alternative investments.

Selling for Tax Reasons Alone

Never let tax considerations completely dictate your investment decisions. Selling a fundamentally strong company just to harvest a small loss might be counterproductive if that company is poised for a rebound. Your investment thesis should always take precedence, with tax-loss harvesting serving as an optimization tool, not the primary driver.

Overlooking Transaction Costs

While often small, brokerage commissions and trading fees can eat into your tax savings, especially if you’re making numerous small trades. Factor these costs into your calculations to ensure the tax benefits outweigh the expenses.

Not Considering All Accounts

The wash-sale rule applies across all your accounts, including taxable brokerage accounts, IRAs, and even accounts held by your spouse. If you sell a stock for a loss in your taxable account and then buy the same stock in your IRA within the 30-day window, the loss will still be disallowed. This often catches investors by surprise.

Missing the December Deadline

All trades must settle by the end of the tax year (December 31st) to be counted for Tax-Loss Harvesting 2026. Due to varying settlement periods (T+2 for most securities), it’s advisable to execute your sales a few days before December 31st to ensure they settle in time. Don’t wait until the last minute!

Advanced Strategies for Tax-Loss Harvesting 2026

For more seasoned investors, there are several advanced strategies that can further optimize your Tax-Loss Harvesting 2026 efforts:

Tax-Loss Harvesting with ETFs and Mutual Funds

ETFs and mutual funds can be excellent candidates for tax-loss harvesting. If you hold an actively managed mutual fund that has underperformed, you can sell it for a loss and reinvest in a similar but not identical index ETF or another actively managed fund with a different investment strategy. This allows you to maintain exposure to a particular asset class while realizing a tax loss. Just be mindful of the ‘substantially identical’ rule when switching between funds that track the same index.

Pairing Gains and Losses

If you have both short-term capital gains and long-term capital gains, you’ll want to be strategic about which losses you harvest. Short-term losses offset short-term gains first, then long-term gains. Long-term losses offset long-term gains first, then short-term gains. Since short-term capital gains are taxed at higher ordinary income rates, using short-term losses to offset them can be particularly beneficial.

Considering Future Tax Brackets

If you anticipate being in a lower tax bracket in the future, it might make sense to carry forward more losses. Conversely, if you expect higher income and thus a higher tax bracket, maximizing your current year’s loss utilization could be more advantageous. This requires some foresight into your financial situation.

Automated Tax-Loss Harvesting

Many robo-advisors and some traditional financial advisors offer automated tax-loss harvesting services. These platforms continuously monitor your portfolio for opportunities to harvest losses, often on a daily basis, and execute trades automatically while adhering to the wash-sale rule. This can be a hands-off way to ensure you’re consistently optimizing your tax situation, especially for investors with diversified portfolios.

The December Deadline: Why Timing is Everything for Tax-Loss Harvesting 2026

The end of the calendar year is the critical period for Tax-Loss Harvesting 2026. All sales must settle by December 31st, 2026, to be counted for that tax year. Given that most stock and ETF trades settle in two business days (T+2), you typically need to execute your sales by the last few trading days of December. Waiting until December 31st is risky, as a trade placed on that day might not settle until January of the following year, causing the loss to apply to your 2027 taxes instead.

It’s advisable to start reviewing your portfolio for potential losses in late November or early December. This gives you ample time to identify suitable candidates, consider reinvestment options, and execute trades without the pressure of a looming deadline. Remember that market conditions can change rapidly, so what looks like a loss opportunity today might not be one tomorrow.

Consulting with a financial advisor or tax professional is particularly beneficial during this period. They can help you analyze your specific tax situation, identify the most impactful harvesting opportunities, and ensure compliance with all IRS regulations, including the complex wash-sale rule across various accounts.

Documenting Your Tax-Loss Harvesting Activities

Proper documentation is essential for accurate tax reporting. Your brokerage statements will typically provide the necessary information, including the date of sale, the proceeds from the sale, and the cost basis of the security, which allows for the calculation of your realized gain or loss. For any wash sales, your brokerage should adjust the cost basis of the replacement security accordingly.

When you file your taxes, you will report your capital gains and losses on IRS Form 8949, Sales and Other Dispositions of Capital Assets, and then summarize them on Schedule D, Capital Gains and Losses. If you have carried-forward losses from previous years, these will also be accounted for on Schedule D. Keeping organized records throughout the year will make this process much smoother.

Conclusion: Maximize Your After-Tax Returns with Proactive Tax-Loss Harvesting 2026

Tax-Loss Harvesting 2026 is more than just a tax trick; it’s a fundamental component of intelligent portfolio management. By strategically realizing capital losses, you can significantly reduce your current and future tax liabilities, rebalance your portfolio, and improve your overall investment discipline. While the wash-sale rule and other complexities require careful attention, the benefits of this strategy far outweigh the effort.

As the December deadline approaches, take the time to review your investment portfolio. Identify underperforming assets, understand your capital gains and losses, and formulate a plan to execute your tax-loss harvesting strategy. Whether you manage your own investments or work with a financial advisor, incorporating Tax-Loss Harvesting 2026 into your annual financial routine can lead to substantial long-term savings and a more robust, tax-efficient portfolio.

Don’t leave money on the table. Start planning your Tax-Loss Harvesting 2026 strategy today to ensure you’re maximizing every opportunity to optimize your financial future.