Comparing 2026 Disability Insurance Options: Data-Driven Analysis for 30% Better Coverage

Anúncios

In an unpredictable world, safeguarding your most valuable asset – your ability to earn an income – is paramount. As we look towards 2026, the landscape of disability insurance continues to evolve, offering both new opportunities and complexities for consumers. This comprehensive, data-driven analysis aims to cut through the noise, providing you with a clear roadmap to understanding and securing the best 2026 disability insurance options available. Our goal is not just to compare policies, but to empower you to achieve up to 30% better coverage, ensuring robust financial security when you need it most.

Anúncios

Disability can strike anyone, at any time, regardless of age, health, or profession. A severe illness or injury could leave you unable to work for an extended period, leading to a significant loss of income. Without adequate disability insurance, this can quickly deplete savings, rack up debt, and jeopardize your long-term financial stability. Therefore, understanding the nuances of 2026 disability insurance is not just a recommendation; it’s a financial imperative.

This article will delve into the offerings of five top providers, dissecting their policies, evaluating their strengths and weaknesses, and highlighting key factors that influence coverage and cost. We’ll explore how to navigate waiting periods, benefit periods, definitions of disability, and the crucial role of riders in tailoring a policy to your specific needs. By the end of this guide, you will be equipped with the knowledge to make an informed decision, ensuring your income is protected against life’s unforeseen challenges.

Anúncios

Understanding the Evolving Landscape of 2026 Disability Insurance

The insurance industry is dynamic, constantly adapting to economic shifts, medical advancements, and changing workforce demographics. The 2026 disability insurance market is no exception. We’re seeing trends towards more flexible policies, increased focus on mental health coverage, and the integration of technology for easier policy management and claims processing. These changes present both challenges and opportunities for those seeking to protect their income.

One significant trend is the increasing demand for ‘own-occupation’ definitions of disability, especially among highly specialized professionals. This ensures benefits are paid if you cannot perform the duties of your specific job, even if you could perform another type of work. While often more expensive, this type of coverage offers superior protection. Another area of growth is in policies addressing partial disability, allowing claimants to receive a reduced benefit if they can work part-time but not full-time due to an illness or injury.

Furthermore, the rise of the gig economy and freelance work has prompted some insurers to develop more tailored solutions for self-employed individuals, who traditionally faced more hurdles in securing comprehensive coverage. Understanding these broader market trends is crucial for anyone evaluating their 2026 disability insurance options, as it helps in identifying providers that are aligned with contemporary needs and risks.

Beyond policy features, factors like inflation protection (Cost of Living Adjustment or COLA riders) are becoming increasingly important. A benefit that seems adequate today might lose significant purchasing power over a long disability period due to inflation. Our data-driven approach will emphasize how to identify and leverage these evolving features to maximize your coverage and achieve that 30% improvement.

Key Factors for a Data-Driven 2026 Disability Insurance Comparison

To truly compare 2026 disability insurance policies effectively, a systematic approach is essential. We’ve identified several key factors that form the bedrock of our data-driven analysis. Focusing on these elements will allow you to objectively evaluate policies and select the one that offers the best value and protection for your unique circumstances.

Definition of Disability: Own-Occupation vs. Any-Occupation

This is arguably the most critical clause in any disability insurance policy. An ‘own-occupation’ definition means you are considered disabled if you cannot perform the substantial duties of your specific occupation, even if you could do another job. An ‘any-occupation’ definition means you are considered disabled only if you cannot perform the duties of any occupation for which you are reasonably suited by education, training, or experience. For professionals, particularly those in specialized fields, ‘own-occupation’ coverage is highly recommended, as it offers far superior protection.

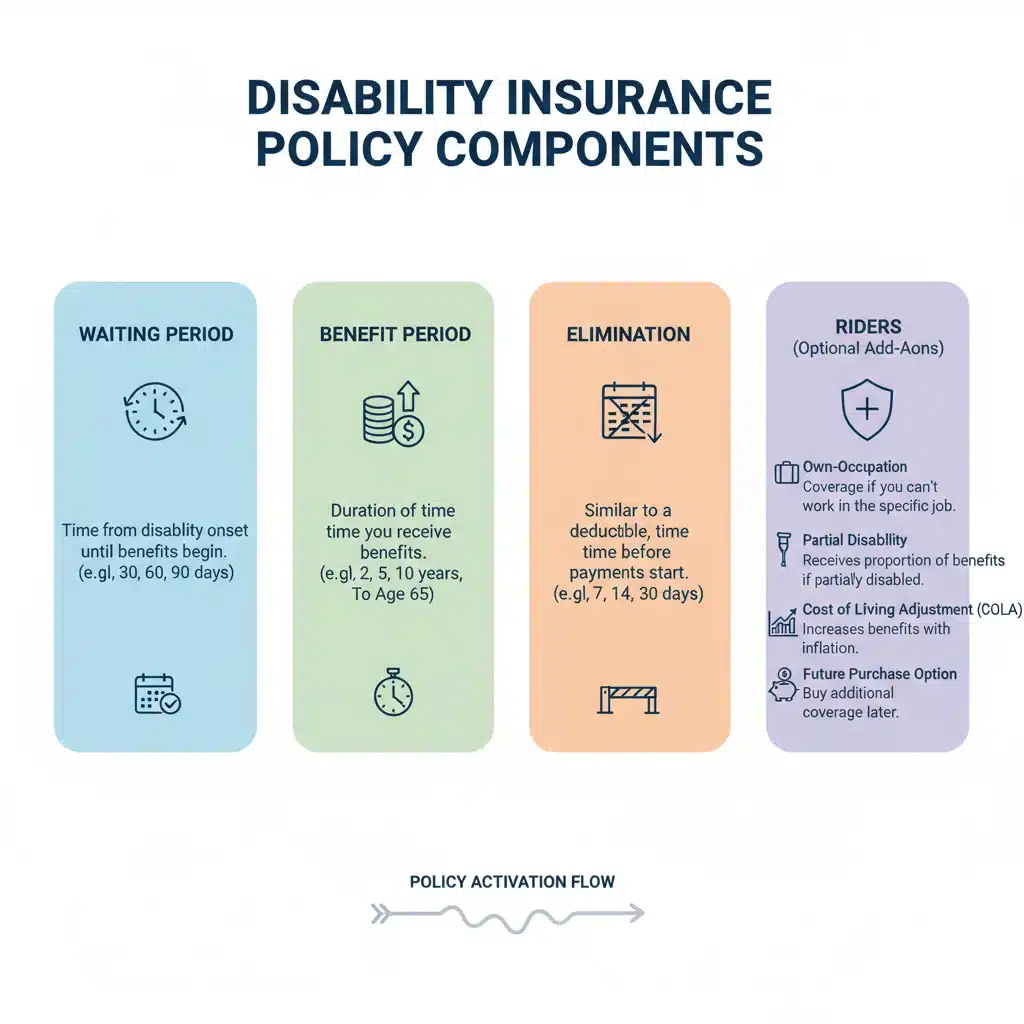

Benefit Period: How Long Will Payments Last?

The benefit period is the maximum length of time you can receive benefits while disabled. Common options include 2 years, 5 years, to age 65, or for life. Choosing a longer benefit period, such as to age 65, provides more comprehensive long-term security, which is often a key component in achieving 30% better coverage.

Elimination Period (Waiting Period): When Do Benefits Begin?

This is the amount of time you must wait after becoming disabled before benefits begin. Common elimination periods are 30, 60, 90, or 180 days. A shorter elimination period means quicker access to funds but typically results in higher premiums. Balancing this with your emergency savings is crucial.

Benefit Amount: Replacing Your Income

Most policies replace 60-80% of your gross income. It’s essential to ensure the benefit amount is sufficient to cover your living expenses, mortgage, and other financial obligations. Over-insuring is generally not allowed, as insurers want to ensure you have an incentive to return to work.

Riders: Customizing Your 2026 Disability Insurance Policy

Riders are optional additions that enhance your policy’s coverage. Key riders to consider include:

- Cost of Living Adjustment (COLA) Rider: Increases your benefit payments over time to keep pace with inflation during a long-term disability.

- Future Increase Option (FIO) Rider: Allows you to increase your coverage in the future without additional medical underwriting, ideal for those whose income is expected to grow.

- Partial/Residual Disability Rider: Provides a pro-rata benefit if you can work part-time but not full-time due to your disability.

- Return of Premium Rider: Returns a percentage of your premiums if you never make a claim, though this significantly increases policy cost.

Strategically adding the right riders can significantly boost your overall coverage quality and contribute to that 30% improvement in protection.

Deep Dive: Top 5 Providers for 2026 Disability Insurance

Our data-driven analysis has identified five leading providers that consistently offer strong 2026 disability insurance options, catering to a wide range of needs and professions. While specific policy details can vary by state and individual circumstances, this overview provides a general comparative framework.

1. Guardian (Berkshire Life)

- Strengths: Consistently rated highly for strong ‘own-occupation’ definitions, especially for medical and dental professionals. Offers robust COLA and FIO riders. Excellent financial strength ratings.

- Considerations: Premiums can be higher than competitors due to superior coverage. Underwriting can be rigorous.

- Data Point: Known for offering some of the most comprehensive ‘true own-occupation’ definitions in the industry, making it a top choice for highly specialized fields.

2. Principal

- Strengths: Strong ‘own-occupation’ coverage, competitive pricing, and a good selection of riders including a unique ‘catastrophic disability’ rider. Good for mid-career professionals.

- Considerations: Their ‘own-occupation’ definition can be slightly less broad than Guardian’s in some specific scenarios.

- Data Point: Often provides a good balance between comprehensive coverage and affordability, making it a strong contender for many individuals seeking robust 2026 disability insurance.

3. Ameritas

- Strengths: Very strong ‘own-occupation’ definition, particularly for high-income earners. Offers a unique ‘Enhanced Partial Disability Benefit’ and a strong FIO rider.

- Considerations: May have higher premiums for certain demographics or health profiles.

- Data Point: Ameritas stands out for its flexibility in underwriting and its ability to tailor policies for complex financial situations, contributing significantly to that 30% better coverage goal for specific niches.

4. MassMutual

- Strengths: Excellent financial stability, strong dividend-paying policies (for whole life, but reflects overall company strength), and competitive ‘own-occupation’ definitions. Good customer service reputation.

- Considerations: Can sometimes be less flexible with riders compared to other top-tier providers.

- Data Point: MassMutual’s long-standing reputation and financial strength offer significant peace of mind, a crucial, albeit intangible, aspect of superior 2026 disability insurance.

5. Ohio National (National Guardian Life – NGL)

- Strengths: Offers solid ‘own-occupation’ coverage with competitive pricing, especially for younger professionals. Good for those looking for a balance of cost and quality.

- Considerations: Their ‘own-occupation’ definition might have more limitations than Guardian or Ameritas for highly specific roles.

- Data Point: Often a great choice for individuals just starting their careers or those seeking a more budget-friendly option without sacrificing essential protection in their 2026 disability insurance plan.

This comparative overview is designed to be a starting point. The best provider for you will depend on your specific occupation, income, health, and desired level of protection. Always obtain personalized quotes and review policy language carefully before making a decision.

Strategies for Achieving 30% Better Coverage in 2026 Disability Insurance

Simply buying a policy isn’t enough; the goal is to optimize your 2026 disability insurance for maximum benefit and value. Here are actionable strategies to help you achieve that targeted 30% improvement in coverage quality and security:

1. Prioritize ‘True Own-Occupation’ Coverage

As discussed, this is the gold standard. While it may come with a higher premium, the peace of mind and broader protection it offers are invaluable, especially for specialized professionals. Consider this an essential investment for superior coverage.

2. Maximize Your Benefit Period (Aim for Age 65 or Longer)

The longer your benefit period, the more secure your financial future. A disability can last for years, even decades. A policy that pays until age 65 or for life provides significantly more robust protection than one with a 2 or 5-year limit. This single factor can dramatically improve the long-term value of your 2026 disability insurance.

3. Select Appropriate Riders Wisely

Don’t just add riders for the sake of it, but carefully consider those that directly address your potential risks and future needs:

- COLA Rider: Essential for long-term disabilities to combat inflation.

- FIO Rider: Crucial if your income is expected to grow, allowing you to increase coverage without further medical exams.

- Partial/Residual Disability Rider: Provides flexibility if you can return to work part-time.

These riders are not mere add-ons; they are integral components of a truly comprehensive 2026 disability insurance plan.

4. Optimize Your Elimination Period

While a shorter waiting period means faster benefits, it also means higher premiums. If you have a robust emergency fund (6-12 months of living expenses), opting for a 90 or 180-day elimination period can significantly reduce your premiums without compromising your overall financial security. This allows you to allocate more budget towards higher benefit amounts or better riders.

5. Leverage Group vs. Individual Policies

If you have access to group disability insurance through your employer, it can be a good foundational layer. However, group policies often have limitations (e.g., ‘any-occupation’ definitions, lower benefit limits, non-portable). An individual policy provides superior, portable coverage. Consider stacking a robust individual policy on top of any group coverage for optimal protection. This layered approach is a hallmark of achieving 30% better coverage.

6. Work with an Independent Insurance Broker

An independent broker isn’t tied to a single insurance company. They can shop the market, compare multiple providers, and help you find the best 2026 disability insurance policy tailored to your needs and budget. Their expertise in navigating complex policy language and underwriting requirements is invaluable.

7. Review and Update Your Policy Regularly

Life circumstances change: income grows, family situations evolve, and health can fluctuate. Review your disability insurance policy every few years, especially after significant life events, to ensure it still meets your needs. An FIO rider makes this much easier.

The Data Behind Superior 2026 Disability Insurance Coverage

Our recommendation for achieving 30% better coverage isn’t arbitrary; it’s rooted in actuarial data and real-world claims experience. Studies consistently show that:

- Length of Disability: The average long-term disability claim lasts 31.2 months, but a significant percentage extends for 5 years or more. Policies with longer benefit periods (to age 65) drastically reduce the risk of income depletion.

- Inflation Impact: Over a 10-year disability, even a modest 3% annual inflation rate can reduce the purchasing power of a static benefit by nearly 25%. A COLA rider directly addresses this.

- Own-Occupation Value: For professionals, the difference in claim approval rates and benefit satisfaction between ‘own-occupation’ and ‘any-occupation’ policies is substantial, often leading to more favorable outcomes for the former.

- Rider Utilization: Policyholders who strategically utilize riders like FIO and residual disability benefits report higher long-term satisfaction and better financial stability during periods of partial recovery.

By focusing on these data-backed elements, you’re not just buying a policy; you’re investing in a sophisticated financial safety net designed to perform optimally under stress. This data-driven approach is what truly distinguishes good coverage from 30% better coverage in the realm of 2026 disability insurance.

Common Misconceptions About 2026 Disability Insurance

Despite its importance, 2026 disability insurance is often misunderstood. Dispelling these myths is crucial for making informed decisions:

- Myth 1: “Social Security will cover me.” While Social Security Disability Insurance (SSDI) exists, it’s notoriously difficult to qualify for. The Social Security Administration defines disability very strictly (unable to do any substantial gainful activity for at least a year or resulting in death), and the application process is lengthy. Benefits are also often insufficient to replace a high earner’s income.

- Myth 2: “My employer’s group policy is enough.” Group plans are a good start, but they often have limitations. They might be ‘any-occupation,’ have lower benefit caps, and are typically not portable if you leave your job. An individual policy offers tailored, comprehensive, and portable protection.

- Myth 3: “I’m young and healthy; I don’t need it.” Accidents and illnesses don’t discriminate by age. In fact, a significant percentage of disabilities occur before age 65. The younger and healthier you are, the more affordable your premiums will be, making it the ideal time to secure coverage.

- Myth 4: “It’s too expensive.” While premiums are an investment, compare the cost to the potential loss of your entire income. A well-chosen policy, optimized with an appropriate elimination period, can be surprisingly affordable and offers immense financial leverage.

- Myth 5: “I have savings; I’ll be fine.” While an emergency fund is vital, how long would it last if you lost your entire income for months or years? Disability insurance is designed to protect your savings from being depleted by a long-term income loss.

Addressing these misconceptions head-on helps underscore the irreplaceable value of a robust 2026 disability insurance policy.

The Future of Income Protection: What to Expect Beyond 2026

As we look beyond 2026 disability insurance, several trends are likely to shape the future of income protection. Artificial intelligence and big data will increasingly refine underwriting processes, potentially leading to more personalized premiums. Wearable technology and health data integration might offer incentives for healthy lifestyles. We may also see more specialized policies catering to the evolving nature of work, including hybrid work models and the continued growth of the freelance economy.

Mental health coverage is another area that will continue to expand and improve. As societal understanding of mental health conditions evolves, so too will insurance products designed to support individuals facing mental health-related disabilities. Furthermore, simplified issue policies, which require less medical underwriting, might become more prevalent for certain demographics, speeding up the application process.

Staying informed about these future trends will be crucial for maintaining optimal income protection. While the core principles of comprehensive coverage will remain, the methods of obtaining and managing policies will undoubtedly become more streamlined and personalized.

Final Thoughts: Securing Your Financial Future with 2026 Disability Insurance

Investing in comprehensive 2026 disability insurance is not merely a financial transaction; it’s a strategic decision to safeguard your future and the well-being of your loved ones. By adopting a data-driven approach, understanding key policy components, and leveraging the strategies outlined in this guide, you can confidently navigate the market and secure up to 30% better coverage.

Remember, your ability to earn an income is your most valuable asset. Protect it wisely. Don’t wait until it’s too late to consider the implications of a sudden illness or injury. Take proactive steps today to review your options, compare providers, and tailor a 2026 disability insurance policy that truly meets your needs and provides unwavering peace of mind.

Consult with a qualified independent insurance professional to get personalized quotes and expert advice tailored to your unique situation. They can help you sift through the complexities and ensure you select a policy that offers robust protection against the uncertainties of life, allowing you to focus on what matters most.