Navigating 2026 COBRA Subsidies: Your 6-Month Coverage Guide

Anúncios

Navigating the 2026 COBRA Subsidy Changes: A Practical Guide to Maintaining Health Coverage for 6 Months

The landscape of health insurance can often feel like a labyrinth, especially when life throws unexpected curveballs like job changes or significant life events. For many, the Consolidated Omnibus Budget Reconciliation Act (COBRA) offers a crucial lifeline, allowing individuals and their families to maintain their employer-sponsored health coverage for a transitional period. As we approach 2026, it’s vital to understand the potential changes and implications for COBRA Subsidy 2026, particularly regarding the duration and scope of financial assistance. This comprehensive guide aims to demystify these upcoming adjustments, providing you with the knowledge to make informed decisions and ensure uninterrupted access to healthcare for up to six months.

Anúncios

Maintaining continuous health coverage is not just about avoiding unexpected medical bills; it’s about peace of mind, access to necessary treatments, and safeguarding your family’s well-being. The potential for COBRA Subsidy 2026 to offer a significant financial reprieve for a limited time makes understanding its nuances absolutely essential. Whether you’re anticipating a job transition, facing a qualifying event, or simply want to be prepared, this article will walk you through the intricacies of COBRA, potential subsidy mechanisms, eligibility requirements, and crucial steps to take.

We will delve into what COBRA is, why subsidies are sometimes necessary, and what specific changes or considerations might arise in 2026. Our focus will be on providing practical, actionable advice, ensuring you can confidently navigate your health coverage options during what can often be a stressful period. Let’s embark on this journey to secure your health future.

Anúncios

Understanding COBRA: The Basics of Continued Coverage

Before we dive into the specifics of COBRA Subsidy 2026, it’s crucial to have a solid understanding of what COBRA entails. Enacted in 1985, COBRA is a federal law that gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances such as voluntary or involuntary job loss, reduction in the hours worked, transition between jobs, death, divorce, and other life events. This means that if you’re covered by an employer-sponsored health plan, you generally have the option to keep that same coverage, even after leaving your job.

Who is Eligible for COBRA?

To be eligible for COBRA, several conditions must be met:

- The plan must be covered by COBRA: Generally, COBRA applies to group health plans maintained by private-sector employers with 20 or more employees on more than 50% of its typical business days in the previous calendar year. It also applies to state and local governments.

- A qualifying event must occur: This is a specific event that causes an individual to lose health coverage. Common qualifying events include:

- Termination of employment (for reasons other than gross misconduct).

- Reduction in hours of employment.

- Death of the covered employee.

- Divorce or legal separation from the covered employee.

- A covered employee becoming entitled to Medicare.

- A child ceasing to be a dependent under the plan rules.

- You must be a qualified beneficiary: This includes the covered employee, their spouse, and dependent children who were covered by the plan on the day before the qualifying event occurred.

How Long Does COBRA Coverage Last?

The duration of COBRA coverage varies depending on the qualifying event:

- 18 months: For termination of employment or reduction of hours.

- 29 months: If a qualified beneficiary is determined to be disabled by the Social Security Administration during the first 60 days of COBRA coverage.

- 36 months: For other qualifying events, such as divorce, death of the employee, or a child losing dependent status.

It’s important to note that while COBRA allows you to continue your exact same health plan, it often comes at a significant cost. Employers typically pay a large portion of employee health insurance premiums. When you elect COBRA, you become responsible for the entire premium, plus an administrative fee of up to 2%, making it considerably more expensive than what you paid as an active employee. This is where subsidies can play a critical role, and why understanding the potential for COBRA Subsidy 2026 is so important.

The Role of Subsidies in COBRA Coverage

The high cost of COBRA is often a barrier for many individuals and families, forcing them to forgo health coverage during a transitional period. This is where government subsidies can come into play, making COBRA more affordable. Historically, there have been periods when federal legislation has provided premium assistance for COBRA coverage, most notably during economic downturns or public health crises.

Past COBRA Subsidies: Lessons Learned

One of the most significant examples of COBRA subsidies was enacted under the American Rescue Plan Act (ARPA) in 2021. This legislation provided a 100% subsidy for COBRA premiums for eligible individuals from April 1, 2021, through September 30, 2021. This was a critical relief measure during the COVID-19 pandemic, helping millions maintain their health coverage without the financial burden.

Key takeaways from past subsidy programs include:

- Targeted Relief: Subsidies are often introduced during specific periods of economic hardship or national emergencies.

- Eligibility Criteria: While general COBRA eligibility applies, subsidy programs often have additional criteria, such as involuntary termination or reduction in hours.

- Limited Duration: Subsidies are typically temporary, designed to provide short-term relief rather than long-term solutions. The focus on a 6-month period for COBRA Subsidy 2026 aligns with this historical pattern.

- Retroactive Application: Some past subsidies allowed for retroactive coverage, meaning individuals could enroll and receive reimbursement for premiums already paid.

These past programs set a precedent for how future subsidies, including any potential COBRA Subsidy 2026, might be structured. Understanding these historical patterns can help us anticipate the design and impact of future legislative actions.

Anticipating COBRA Subsidy 2026: What to Expect

As of now, there is no standing federal legislation mandating a COBRA Subsidy 2026. However, discussions and proposals around healthcare affordability are ongoing. The focus on a 6-month duration suggests a potential scenario where a short-term, targeted subsidy might be introduced, similar to past relief efforts. Such a subsidy would likely be a response to specific economic conditions, public health concerns, or broader healthcare reform initiatives.

Potential Triggers for a 2026 Subsidy

Several factors could potentially trigger the introduction of a COBRA Subsidy 2026:

- Economic Downturn: A significant economic recession or widespread job losses could prompt legislative action to support displaced workers.

- Healthcare Policy Changes: Broader reforms in healthcare policy, aimed at increasing access and affordability, might include COBRA premium assistance as a component.

- Public Health Crises: While hopefully not on the horizon, another major public health crisis could necessitate a rapid response, including health coverage support.

- Political Initiatives: New administrations or shifts in congressional priorities could lead to proposals for temporary COBRA subsidies as part of their agenda.

It’s crucial to monitor legislative developments and news from government agencies like the Department of Labor (DOL) and the Department of Health and Human Services (HHS) for any announcements regarding COBRA Subsidy 2026. These agencies typically provide detailed guidance on eligibility and application processes once such legislation is enacted.

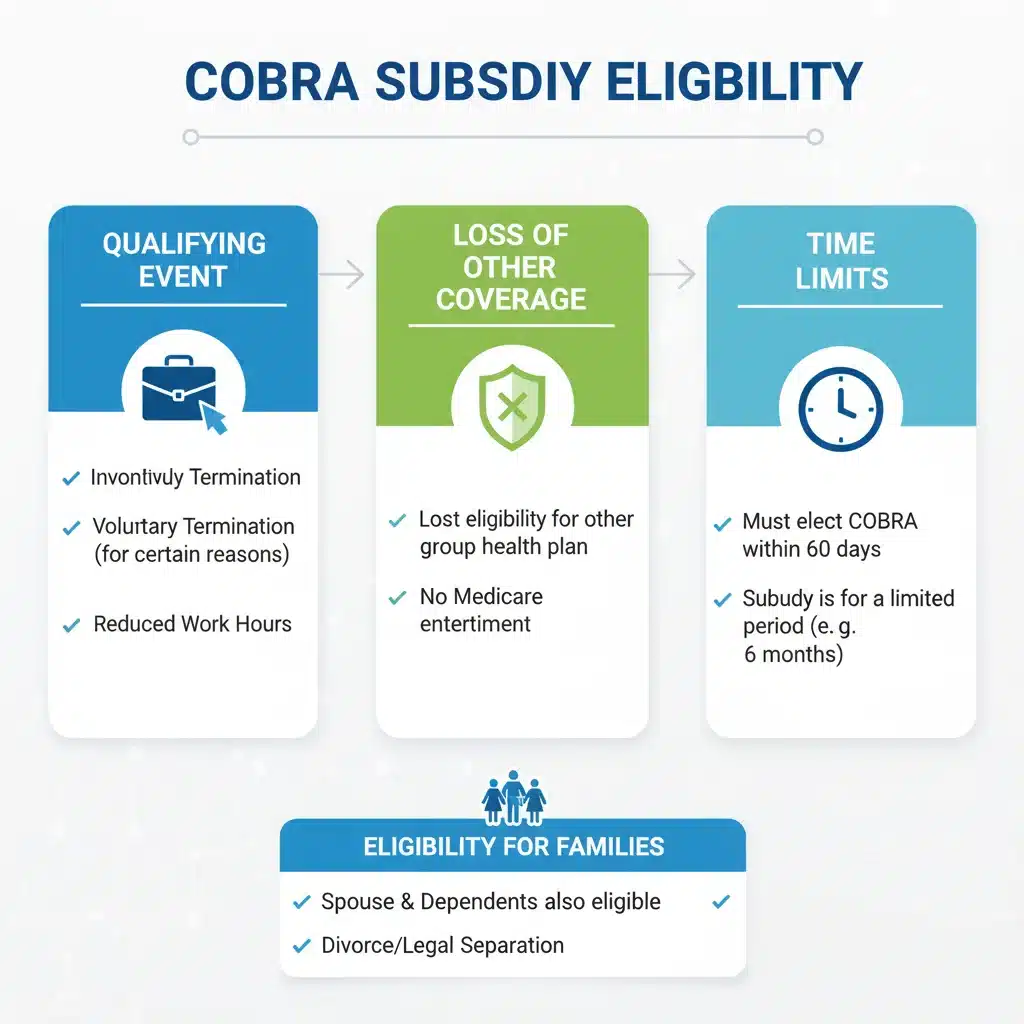

Eligibility for a Potential 6-Month COBRA Subsidy in 2026

While the specifics of any COBRA Subsidy 2026 are yet to be defined, we can infer potential eligibility criteria based on past programs and the nature of such relief efforts. The emphasis on a 6-month duration suggests a focus on individuals experiencing short-term disruptions in employment.

Key Eligibility Factors (Based on Historical Precedent):

If a COBRA Subsidy 2026 were to be enacted, it would likely include:

- Qualifying Event: The most common qualifying events for subsidized COBRA have been involuntary termination of employment or reduction in hours. It’s less likely that events like divorce or a child aging out would qualify for a temporary subsidy, as these are not directly tied to economic displacement.

- Not Eligible for Other Group Coverage: Individuals would typically not be eligible for the subsidy if they become eligible for other group health plan coverage (e.g., through a new employer or a spouse’s employer) or Medicare. The subsidy is designed to bridge a gap, not provide an alternative to other available coverage.

- Election of COBRA: You must elect COBRA coverage to receive the subsidy. The subsidy would apply to your COBRA premiums, not to other forms of health insurance.

- Specific Timeframe: The subsidy would only apply to COBRA coverage within a designated timeframe, such as the proposed 6-month window in 2026. Coverage outside this window would be at full cost.

- Employer Size: The employer’s size (20+ employees) would still apply for the plan to be COBRA-eligible in the first place.

Actionable Steps for Potential Eligibility:

Even without concrete legislation, you can prepare by:

- Understanding Your Current Plan: Know if your employer’s plan is COBRA-eligible.

- Keeping Records: Maintain records of your employment termination or reduction in hours, as these documents would be crucial for establishing eligibility.

- Monitoring Communications: Pay close attention to communications from your former employer and plan administrator regarding COBRA election notices and potential subsidy information.

The precise details of any COBRA Subsidy 2026 will be critical, particularly the definition of ‘involuntary termination’ and any income limitations that might be imposed. It’s important to remember that these are projections based on past patterns, and actual legislation could differ significantly.

The 6-Month Window: What Does it Mean for You?

The emphasis on a 6-month duration for a potential COBRA Subsidy 2026 is highly significant. This specific timeframe suggests a targeted approach to providing temporary financial relief, designed to help individuals transition between jobs or overcome short-term financial hurdles without losing critical health coverage.

Strategic Implications of a 6-Month Subsidy:

- Bridge to New Employment: A 6-month subsidy can be a lifesaver for those actively seeking new employment with benefits. It provides enough time to find a new job and for their new employer’s health benefits to kick in, without the stress of exorbitant COBRA costs.

- Time to Explore Alternatives: This period also gives individuals ample time to research and enroll in alternative health coverage options, such as those available through the Health Insurance Marketplace (Healthcare.gov) or a spouse’s plan.

- Financial Relief: For individuals facing economic uncertainty, eliminating the high cost of COBRA premiums for six months can free up significant financial resources, allowing them to focus on other essential needs.

- Continuation of Care: For those undergoing ongoing medical treatments or managing chronic conditions, a 6-month subsidy ensures continuity of care with their existing doctors and specialists, avoiding disruptions that can arise from switching insurance plans.

Maximizing the 6-Month Benefit:

If a COBRA Subsidy 2026 becomes available for a 6-month period, here’s how you can make the most of it:

- Elect COBRA Promptly: Upon receiving your COBRA election notice, act quickly. There are strict deadlines for electing COBRA, and missing them can mean losing your eligibility for both COBRA and any associated subsidy.

- Understand the Start Date: Clarify when the 6-month subsidy period begins and ends. This will help you plan your next steps for health coverage.

- Actively Seek New Coverage: Use the 6-month window to actively search for new employment with benefits or explore plans on the Health Insurance Marketplace. Don’t wait until the subsidy is about to expire.

- Budget for Post-Subsidy Costs: If you anticipate needing COBRA beyond the 6-month subsidized period, start planning for the full premium costs.

The 6-month timeframe is a critical component of any potential COBRA Subsidy 2026, offering a strategic window for individuals to maintain health security during significant life transitions.

COBRA vs. Marketplace: Weighing Your Options with a Subsidy

Even with a potential COBRA Subsidy 2026 for six months, it’s essential to compare COBRA with other health insurance options, primarily those available through the Health Insurance Marketplace (Healthcare.gov). While subsidized COBRA can be very attractive due to its continuity of coverage, it might not always be the best long-term solution.

Advantages of Subsidized COBRA:

- Continuity of Care: You keep your existing doctors, specialists, and prescription drug formularies, which is a major benefit, especially for those with ongoing medical needs.

- Familiarity: You remain with the same plan you’re used to, avoiding the learning curve of a new insurance policy.

- No New Deductibles/Out-of-Pocket: If you’ve already met a significant portion of your deductible or out-of-pocket maximum with your employer’s plan, that progress carries over with COBRA.

Considerations for Subsidized COBRA:

- Limited Duration: The 6-month subsidy is temporary. After it ends, you’ll be responsible for 100% of the premium plus the administrative fee, which can be very expensive.

- Future Options: While you have COBRA, you might miss out on certain Special Enrollment Periods (SEPs) for the Marketplace that are tied to the loss of *unsubsidized* coverage. However, losing eligibility for a COBRA subsidy *is* typically a qualifying event for an SEP on the Marketplace.

The Health Insurance Marketplace (ACA Plans):

The Marketplace offers individual and family health plans, and many people are eligible for premium tax credits (subsidies) based on their income. These subsidies can significantly reduce monthly premiums, sometimes making Marketplace plans more affordable than even subsidized COBRA, especially if your income has decreased.

Advantages of Marketplace Plans:

- Income-Based Subsidies: Premium tax credits can make plans very affordable, and cost-sharing reductions can lower deductibles and out-of-pocket maximums for eligible individuals.

- Variety of Plans: You can choose from different metal levels (Bronze, Silver, Gold, Platinum) with varying levels of coverage and cost-sharing.

- Special Enrollment Periods: Loss of job-based coverage (even if you decline COBRA) is a qualifying event for an SEP, allowing you to enroll in a Marketplace plan outside of the annual Open Enrollment Period.

Considerations for Marketplace Plans:

- New Providers: You may need to find new doctors and specialists if your current ones are not in the network of the Marketplace plan.

- New Deductibles: You’ll start fresh with a new deductible and out-of-pocket maximum.

- Plan Choice: The range of plans and networks can vary significantly by location.

Making Your Decision:

If a COBRA Subsidy 2026 is available, your decision will likely involve a careful calculation:

- How long do you expect to be without employer-sponsored coverage? If it’s truly a short gap (e.g., 1-3 months), subsidized COBRA might be ideal. If it’s longer, even up to 6 months, you need to consider the cost after the subsidy ends.

- What are your healthcare needs? If you have ongoing treatments or specific doctors you want to keep, subsidized COBRA offers continuity.

- What is your estimated income for the year? This will determine your eligibility for Marketplace subsidies.

- Compare the Net Costs: Calculate the total cost of subsidized COBRA for 6 months, plus any potential subsequent full-cost COBRA, versus the subsidized cost of a Marketplace plan for the same period.

It’s often wise to explore both options simultaneously. Get a quote for COBRA (with any potential subsidy applied) and also visit Healthcare.gov to see what plans and subsidies you might qualify for. This dual approach ensures you make the most financially sound and medically appropriate decision for your situation.

Practical Steps to Take When Facing a Qualifying Event

Regardless of whether a COBRA Subsidy 2026 is in effect, navigating the period after a qualifying event requires proactive steps to secure your health coverage. Being prepared can alleviate significant stress and prevent gaps in care.

1. Understand Your COBRA Rights and Options:

- Receive Your COBRA Election Notice: Your employer (or plan administrator) is legally required to provide you with a COBRA election notice within 14 days after the plan administrator receives notice of your qualifying event. Read this document carefully.

- Know Your Deadlines: You typically have at least 60 days from the date of the notice (or the date your coverage would end, whichever is later) to elect COBRA. Do not miss this deadline.

- Inquire About Subsidies: If a COBRA Subsidy 2026 is enacted, your election notice should include information on how to apply for it. If not, proactively ask your former employer or plan administrator.

2. Explore Health Insurance Marketplace Plans:

- Visit Healthcare.gov: As soon as you experience a qualifying event, visit the Health Insurance Marketplace. Losing job-based coverage triggers a Special Enrollment Period (SEP), allowing you to enroll in a new plan within 60 days before or after your coverage loss.

- Estimate Your Income: Use the Marketplace tools to estimate your expected household income for the year. This is crucial for determining your eligibility for premium tax credits and cost-sharing reductions.

- Compare Plans: Review the available plans in your area, paying close attention to premiums, deductibles, out-of-pocket maximums, network coverage (doctors and hospitals), and prescription drug formularies.

3. Consider Other Coverage Options:

- Spouse’s Plan: If your spouse has employer-sponsored health coverage, losing your job-based coverage is typically a qualifying event that allows you to enroll in their plan.

- Medicaid: Depending on your income and state of residence, you might qualify for Medicaid, which provides comprehensive, low-cost coverage.

- Short-Term Plans: While not ACA-compliant and offering limited benefits, short-term plans can be a temporary bridge if you’re healthy and anticipate a very brief gap in coverage. Use with extreme caution and understand their limitations.

4. Document Everything:

- Keep copies of all correspondence related to your COBRA election, subsidy applications, and Marketplace enrollments.

- Note down dates, times, and names of people you speak with regarding your health coverage.

5. Seek Expert Advice:

- If you’re unsure about your options, consider consulting with a benefits administrator, an insurance broker, or a navigator from the Health Insurance Marketplace. They can provide personalized guidance based on your specific situation.

By taking these proactive steps, you can ensure a smoother transition and maintain continuous health coverage, whether through COBRA Subsidy 2026 or another suitable option.

The Broader Impact of COBRA Subsidies on Healthcare Access

The discussion around COBRA Subsidy 2026 extends beyond individual financial relief; it touches upon broader issues of healthcare access, economic stability, and public health. When individuals lose their jobs, the immediate concern often shifts to financial stability, and health insurance can become an unaffordable luxury, leading to delayed care or avoidance of necessary medical attention. This can have ripple effects throughout the healthcare system and society at large.

Preventing Gaps in Care:

Subsidies for COBRA play a crucial role in preventing gaps in health coverage. Uninsured periods can lead to:

- Worsening Health Conditions: Individuals may postpone doctor visits, skip medications, or delay necessary procedures, leading to more severe and costly health problems down the line.

- Increased Emergency Room Use: Without primary care, people often resort to emergency rooms for non-urgent conditions, which is the most expensive form of healthcare.

- Medical Debt: Even a minor health issue can quickly lead to substantial medical debt for the uninsured, impacting their financial recovery after job loss.

By making COBRA more affordable, subsidies encourage continuous coverage, ensuring that people can continue to receive preventive care, manage chronic diseases, and address new health concerns promptly. This not only benefits the individual but also contributes to a healthier population and reduces the strain on emergency services.

Economic Stability:

The economic impact of COBRA subsidies is also significant. When people are not burdened by overwhelming healthcare costs, they are better positioned to:

- Re-enter the Workforce: Reduced financial stress allows individuals to focus on job searching and skill development, contributing to a faster economic recovery.

- Maintain Financial Security: Avoiding medical debt helps families maintain their savings and assets, preventing a downward spiral into poverty.

- Boost Consumer Confidence: Knowing that a safety net exists for health coverage can instill greater confidence during periods of economic uncertainty.

Therefore, any potential COBRA Subsidy 2026 is not just a healthcare policy but also an economic one, aimed at stabilizing households and supporting broader economic recovery.

Policy Debates and Future Outlook:

The debate around COBRA subsidies often centers on their cost, effectiveness, and whether they are the most efficient way to achieve healthcare access. Critics may argue that such subsidies are temporary fixes and that resources should be directed towards more permanent solutions, such as strengthening the Affordable Care Act (ACA) Marketplace or expanding Medicaid.

However, proponents emphasize the immediate relief and continuity of care that COBRA subsidies provide, especially during unforeseen crises. The 6-month duration often discussed for COBRA Subsidy 2026 reflects an attempt to balance these concerns, offering targeted, short-term assistance without creating a permanent entitlement program.

As we move towards 2026, the discussions around healthcare affordability and access will undoubtedly continue. The lessons learned from past subsidy programs and the ongoing needs of the population will shape any future legislative actions. Staying informed and advocating for policies that support continuous health coverage remains paramount.

Conclusion: Preparing for Your Health Coverage Future

The prospect of COBRA Subsidy 2026 offering a 6-month window of financial assistance for health coverage is a significant topic for anyone potentially facing a qualifying life event. While specific legislation is yet to be confirmed, understanding the mechanisms of COBRA, the historical context of subsidies, and alternative health coverage options is crucial for proactive planning.

The core message remains: do not let a lapse in employment or a change in life circumstances lead to a lapse in your health coverage. Whether through a potential COBRA Subsidy 2026, the Health Insurance Marketplace, or a spouse’s plan, there are avenues to ensure you and your family remain protected.

Here’s a recap of key takeaways:

- Stay Informed: Monitor news from government agencies and reputable healthcare resources for updates on any COBRA subsidy legislation.

- Know Your COBRA Rights: Understand eligibility, election deadlines, and the full cost of COBRA.

- Evaluate All Options: Always compare COBRA (subsidized or not) with Marketplace plans, Medicaid, and spousal coverage to find the most cost-effective and suitable plan for your needs.

- Act Promptly: Timeliness is critical when electing COBRA or enrolling in Marketplace plans during a Special Enrollment Period.

- Document Everything: Keep meticulous records of all communications and decisions related to your health insurance.

The journey through healthcare options can be complex, but with the right information and a proactive approach, you can navigate these challenges effectively. The potential for a COBRA Subsidy 2026 for 6 months offers a glimmer of hope for many, providing a vital bridge during times of transition. By being prepared, you empower yourself to make the best decisions for your health and financial well-being.